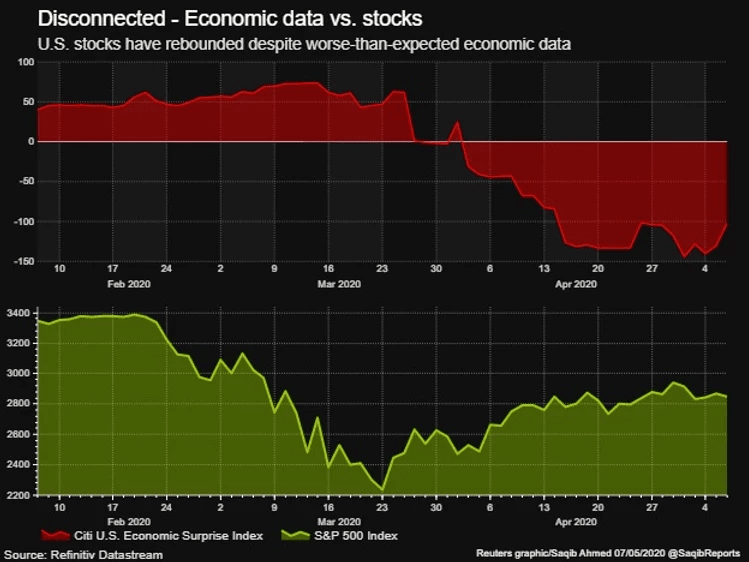

Last Friday saw 20.5mln US jobs lost in the month of April, wiping out a decade of job growth and yet stocks rallied. That statement really says it all about financial markets in the current context.

This week we could see this pattern continue as US Retail Sales are expected to fall 10% in April, exceeding the record 8.4% decline seen in March and Industrial Production is anticipated to fall over 11.5%. However, these economically shocking numbers are likely to be superseded by the anticipation of the gradual lifting of lockdown measures around the world as governments look to resuscitate their domestic economies.

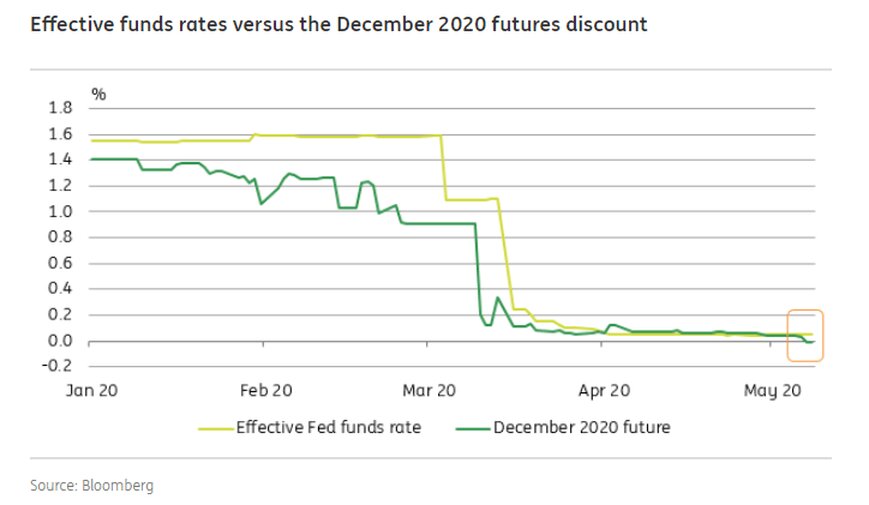

For those not familiar with how this all works, in short, negative rates would punish banks for leaving excess cash with the central bank and thus forcing them to lend which in turn boosts business investment and consumer spending. Read the full explainer HERE.

Although last week's development is symbolic, most of the bank reports I've read this weekend seem to suggest the actual implementation of negative rates by the Federal Reserve is highly unlikely given the disappointing performance in Japan and the Euro-zone and with better economic bang for your buck coming via fiscal expansion.

Nonetheless, Fed Chair Jerome Powell is scheduled to deliver a speech on 'current economic issues' at the Peterson Institute for International Economics this Wednesday which will be one of the main events for the week (full Fed speaker in calendar highlights).

THE EU STRIKES BACKThe European Commission could open a legal case against Germany over a ruling by the country’s constitutional court that the European Central Bank had overstepped its mandate with bond purchases, the EU executive arm said on Sunday. This comes after a German court in Karlsruhe last Tuesday gave the ECB three months to justify its flagship Euro-zone stimulus scheme or said the Bundesbank might have to quit it.

When I tweeted this headline on Saturday I had quite the vocal response on people's thoughts on the longevity of the Euro but from a market point of view I don't think it's a big deal for the immediate future. I base this on the regular legal process on when being the recipient of such demands as we saw last week and that the EU need to adopt a firm stance to discourage other national courts doing the same.

CALENDAR HIGHLIGHTSMonday: JN BoJ Summary of Opinions, IT Industrial Production, US CB Employment Trends Index, 3-yr Auction, Fed's Bostic Speaks

Tuesday: JN Leading Index, 10-yr Auction, CN CPI/PPI, AU NAB Business Confidence, US CPI, Real Earnings, NFIB Small Business Optimism, WASDE Report, 10-yr Auction, Federal Budget Balance, Weekly API Inventories, 10-yr Auction Fed's Harker, Quarles, Mester, Bullard, Kashkari to Speak

Wednesday: JN Bank Lending, Current Account, Economy Watchers Current Index, AU RBNZ Interest Rate Decision (0.25%), Press Conference, AU Westpac Consumer Sentiment, Wage Price Index, IT 3/7/30-yr Auction, GE 30-yr Auction, EU Industrial Production, UK Q1 GDP (P), Business Investment, Construction Output, Industrial/Manufacturing Production, Trade Balance, NIESR GDP Estimate (tentative), US PPI, Weekly DoE Inventories, 30-yr Auction, WR OPEC Monthly Report, Fed's Powell Discusses Current Economic Conditions

Thursday: JN M2/M3 Money Supply, Machine Tool Orders, 30-yr Auction, AU Employment Chance, Unemployment Rate, NZ MI Inflation Expectations, Budget Balance, FR Unemployment Rate, Trade Balance, SP/GE CPI, UK 10-yr Auction, US Weekly Jobless Claims, Import/Export Price Index, CA Manufacturing Sales, BoC Financial System Review, BoC Poloz Speaks, Fed's Kashkari, Kaplan Speak

Friday: JN PPI, CN Industrial Production, Retail Sales, Unemployment Rate, Fixed Asset Investment, IT Industrial Sales/New Orders, CPI, FR CPI, GE GDP, PPI, EU GDP, Employment Change, Trade Balance, US Retail Sales, NY Empire Manufacturing Index, Industrial/Manufacturing Production, JOLTs Job Openings, Michigan Consumer Sentiment, Baker Hughes Rig Count, TIC data

You can find out more information about Amplify Trading HERE.

Have a good week ahead and stay safe.

Anthony Cheung

Head of Market Analysis

(

@AWMCheung)

99% said it helped them gain better knowledge of markets

99% said it helped them gain better knowledge of markets

+44 (0) 203 372 8415

+44 (0) 203 372 8415

info@amplifyme.com

info@amplifyme.com